Have you ever heard someone say, “The rupee is falling against the dollar”? It might sound like financial jargon, but it actually has a very real impact on your day-to-day expenses – even if you’re not travelling abroad. Let’s break it down.

Every country has its own currency. When countries trade with each other, they need to convert their currency into the other’s. So, for example, if India wants to buy something from the US – like crude oil, electronics or machinery – it has to pay in US dollars, not rupees.

Today, 1 US dollar = Rs 75. But next month, 1 US dollar = Rs 80.

This means the rupee has weakened, depreciated or lost value compared to the dollar. Earlier, India needed Rs 75 to buy something worth $1. Now, it needs more rupees, that is, Rs 80, to buy the same thing. That extra Rs 5 has to come from somewhere – and that “somewhere” is your wallet.

So, when the rupee weakens, imports become more expensive, because we need more rupees to buy the same goods from abroad. And since India imports many essential items, like fuel, cooking oil, smartphones, and electronics, those prices go up for everyone. This increase in prices contributes to overall inflation.

Think of it like shopping at a store where the price tag is in dollars. If your rupees are worth less each week, you’ll have to spend more to buy the same things.

That’s why economists and policymakers closely watch the exchange rate. A weak rupee can make imported goods expensive, and that, in turn, can raise prices across the economy – even for things made in India, because transport and input costs can go up.

Why does a falling rupee make your grocery bill heavier?

Because when imported goods and transport get pricier, those costs ripple through the entire supply chain. When the rupee drops, even your shampoo bottle, bus ticket or smartphone can feel the pinch.

So … What does the exchange rate have to do with the price of milk? If fuel prices rise due to a weaker rupee, transport costs go up and, suddenly, your morning milk costs Rs 2 more.

Inflation refers to the rate at which the prices of goods and services rise over time. In India, this is most commonly measured using the consumer price index (CPI). It is a statistical measure that captures the average change in prices of a fixed basket of items, such as food, fuel, clothing, housing and healthcare, that households typically consume. The base year, currently 2012, is assigned a CPI value of 100. All subsequent values show how much prices have risen since that year.

CPI in 2024: 190. CPI in 2025: 194

This means that prices in 2025 were 94% higher than in 2012. But to find inflation for one year, we look at the rate of change between the two years:

So, inflation is 2.11%, even though the CPI level is 194. The CPI tells us prices are almost double what they were in 2012, but the year-on-year increase is what we refer to when we say that inflation is 2.11%.

The Ministry of Statistics and Programme Implementation (MoSPI) publishes CPI data every month. The RBI monitors it closely to make interest rate decisions. If CPI rises sharply, even due to something like a tomato price spike, it can prompt the RBI to raise interest rates, which affects loans, EMIs, savings returns and overall economic activity.

Can everyday consumers affect global inflation?

Absolutely. When millions of people suddenly start spending more (like after the Covid-19 lockdowns), businesses struggle to keep up with demand. As we saw earlier, this pushes prices higher and is known as ‘demand-pull inflation’. For example, when Americans began “revenge spending” in 2021, global supply chains couldn’t catch up, which drove up the prices of electronics, furniture, fuel and even shipping containers. What you buy, how much and when – these choices affect the entire economy.

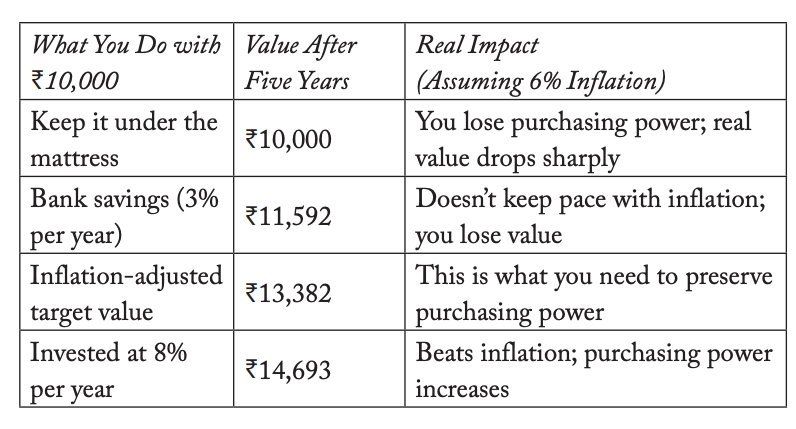

Now let’s bring this back to your wallet. Where does Rs 10,000 go in five years?

Similarly, suppose you save Rs 5,000 every month for ten years in a savings account that earns 3% interest. By the end of ten years, you’ll have saved about Rs 7 lakhs. Sounds like a decent amount, right?

But now imagine inflation has averaged 6% during that time. To buy the same things you could have bought with Rs 7 lakhs ten years ago, you would now need over ₹9 lakhs.

So even though your savings have grown in number, their real value has shrunk. That’s the silent, invisible power of inflation – it eats into your future, rupee by rupee.

And this affects your dreams:

The house you planned to buy: Now out of reach.

The college education you thought you’d covered: Now costs double.

The retirement you hoped would be peaceful: Suddenly feels uncertain.

This is why just saving isn’t enough. You need to make your money grow faster than inflation, and that means you’ll need to invest. But every investment carries uncertainty. Risk isn’t something to fear; it’s something to understand.

Excerpted with permission from The Economy Is Personal: How Big Economic Forces Shape Your Money – And What You Can Do About It, Nupur Pavan Bang and Anisha Sircar, Westland.