The rise and rise of e-commerce in India has changed how people shop in Asia’s third largest economy.

Some even wondered whether the phenomenal success of websites like Flipkart and Snapdeal would threaten the future of brick-and-mortar stores in the country. But things don’t look that bad for traditional retail after all.

Research into 24 large brick-and-mortar retailers in India by credit ratings agency CRISIL shows that these firms will grow at between 13% and 15% over the next two to three years.

“Our study shows revenues have leaped at a very healthy 24% compound annual growth rate to Rs 70,000 crore in the last five years to fiscal 2015 for these two dozen retailers, despite the headwinds,” CRISIL said.

That compares with about 60% growth for online retailers – with an estimated Rs 40,000 crore worth of total goods sold for fiscal 2015 –driven by large discounts and shopping convenience, the report added.

Survival strategy

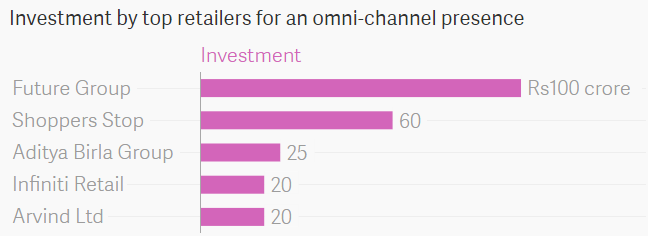

Brick-and-mortar retailers are holding their ground by focusing on tier II and tier III cities, expanding to multiple channels of sales and concentrating more on profitability than revenue growth.

Here’s how the distribution of stores in these cities has changed for five retailers analysed by CRISIL. These include Avenue Supermarts, which operates the D’Mart stores, Shoppers Stop, Hypercity Retail, Lifestyle International and V-Mart Retail.

Going forward, according to CRISIL, online retail could still trump offline for certain product categories like books, music and consumer durables.

Overall, however, online retail will form a small percentage of India’s total retail pie, Arvind Singhal, chairman of management consultancy firm, Technopak, wrote last year:

This article was originally published on qz.com.

We welcome your comments at

letters@scroll.in.

Some even wondered whether the phenomenal success of websites like Flipkart and Snapdeal would threaten the future of brick-and-mortar stores in the country. But things don’t look that bad for traditional retail after all.

Research into 24 large brick-and-mortar retailers in India by credit ratings agency CRISIL shows that these firms will grow at between 13% and 15% over the next two to three years.

“Our study shows revenues have leaped at a very healthy 24% compound annual growth rate to Rs 70,000 crore in the last five years to fiscal 2015 for these two dozen retailers, despite the headwinds,” CRISIL said.

That compares with about 60% growth for online retailers – with an estimated Rs 40,000 crore worth of total goods sold for fiscal 2015 –driven by large discounts and shopping convenience, the report added.

Survival strategy

Brick-and-mortar retailers are holding their ground by focusing on tier II and tier III cities, expanding to multiple channels of sales and concentrating more on profitability than revenue growth.

Here’s how the distribution of stores in these cities has changed for five retailers analysed by CRISIL. These include Avenue Supermarts, which operates the D’Mart stores, Shoppers Stop, Hypercity Retail, Lifestyle International and V-Mart Retail.

Going forward, according to CRISIL, online retail could still trump offline for certain product categories like books, music and consumer durables.

Overall, however, online retail will form a small percentage of India’s total retail pie, Arvind Singhal, chairman of management consultancy firm, Technopak, wrote last year:

Firstly, total consumer spending is dominated by food—and of that, more than 50% is accounted for by perishables that include dairy, vegetables, meat, and fruit.

Secondly, almost 50% of the total consumer spending is still spread across the entire rural India where it is yet not likely that e-tail will make a big impact (while e-commerce would comprising of services such as financial, entertainment, information and education etc.).

And the most important impact categories for e-tail—consumer electronics, durables and appliances, apparel and footwear, and furniture—account for just about 18% of the total consumer spending on merchandise.

This article was originally published on qz.com.